IMF: Financial System's Calm Response to Middle East War Masks Amplification Risks, Especially in Private Credit and Nonbanks

The IMF's April 2026 Global Financial Stability Report argues that the orderly market response to the Middle East war reflects resilience that 'should not be taken at face value' — and that elevated nonbank leverage, equity-market concentration, tight credit spreads, and opaque private credit create amplification channels that could turn future shocks into acute stress.

The International Monetary Fund's April 2026 Global Financial Stability Report, released April 14 at the Fund's Spring Meetings in Washington, warns that the global financial system's outwardly orderly response to the Middle East war reflects a resilience that "should not be taken at face value."

The headline of the report — "Global Financial Markets Confront the War in the Middle East and Amplification Risks" — tracks two parallel stories: markets absorbed the initial shock, and the capacity for that absorption is less robust than the tape suggests.

What the report says

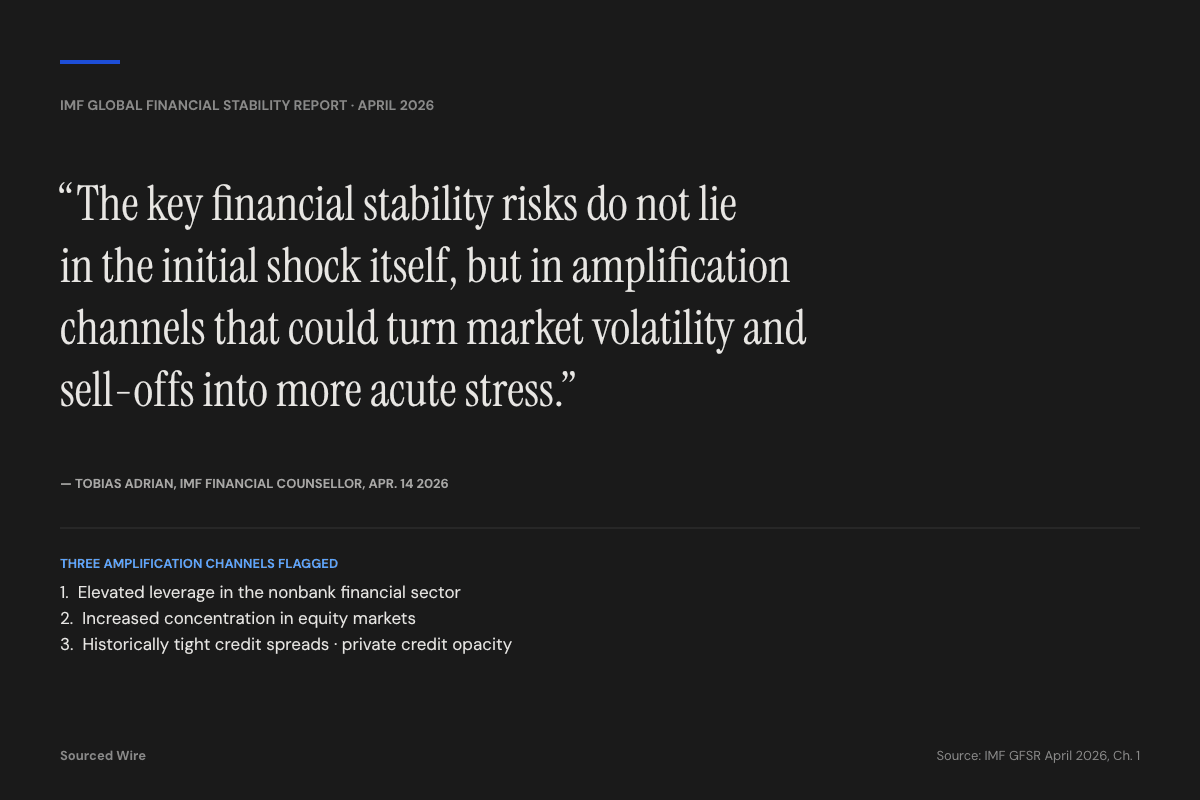

The GFSR's core argument, distilled in the accompanying IMF blog by Financial Counsellor Tobias Adrian:

The key financial stability risks do not lie in the initial shock itself, but in amplification channels that could turn market volatility and sell-offs into more acute stress.

Three such channels are singled out:

- Elevated leverage in parts of the nonbank financial sector — including hedge funds and investment funds that the Fund identifies as "more sensitive" to shifts in global risk than other institutional investors.

- Increased concentration in equity markets — concentration that could magnify drawdowns if confidence breaks.

- Historically tight credit spreads — tight spreads mean limited cushion before spread widening becomes disorderly.

Layered on top, the report flags private credit as "an important area of focus." Rapid growth in direct lending has made the sector systemic, while "opacity, valuation practices, short-term funding backed by longer-term assets, and rising defaults pose challenges."

Why the calm is misleading

The IMF frames the current calm as a function of three things that are not necessarily durable:

| Factor | What the GFSR says |

|---|---|

| Cycles of escalation and de-escalation | Markets have priced the conflict as a series of shocks, not a single regime change |

| Structural improvements in the financial system | Core market infrastructure and short-term funding markets functioned through the stress |

| Absence of a decisive adverse turn | "Markets have not fully priced adverse scenarios" |

And it notes explicitly that orderly price adjustment has been the exception in recent history, not the rule:

Financial conditions have tightened since the onset of the conflict, but they remain far from the stress levels observed during past episodes of global turmoil. Compared with earlier crises, there is still a considerable margin of safety.

The transmission: inflation and yield curves

The primary channel by which the Middle East war has reached balance sheets has been inflation expectations. Higher energy prices have pushed breakeven inflation rates and yields up across advanced and emerging economies. Yield curves have flattened — short-term rates rising faster than long-term rates — which the IMF frames as "a difficult environment facing central banks."

The report pushes a specific implication: "monetary policy must remain focused on price stability" in the short term, while persistent flattening may signal growth damage from the prolonged war.

Emerging markets and the investor base

The report singles out a structural shift in sovereign debt markets. As central bank balance sheets contract (quantitative tightening), the marginal buyer of government debt is increasingly a "price-sensitive nonbank investor" — a dynamic that can cause sovereign yields to "respond more forcefully to inflation shocks than in the past."

Emerging markets face an amplified version of the same dynamic: "Elevated pre-shock valuations and the growing dominance of debt portfolio flows and carry-trade strategies have increased exposure to global risk sentiment."

Policy space

The GFSR contrasts the space available across policy domains:

- Monetary policy: constrained — must hold the line on inflation even as the war hurts growth.

- Fiscal policy: constrained — high debt and persistent deficits limit response.

- Financial stability policy: less constrained — central bank balance sheets have room to expand for asset purchases if needed; crisis-management frameworks and liquidity backstops are "stronger than in the past."

The Fund's concluding instruction to policymakers: "Prepare, don't predict."

Resilience should not be inferred from the absence of stress. Elevated asset prices, intact risk-taking incentives, and stronger amplification channels mean that risks remain skewed to the downside — even if markets have adjusted in an orderly manner so far.