Justin Sun Sues Trump Family's World Liberty Financial, Alleges Secret 'Blacklist' Backdoor Froze His $1B in Tokens

Tron founder Justin Sun's anchor $45M investment helped World Liberty go from a $22M-in-its-first-month flop to a $550M raise. His new complaint says WLF then secretly modified the smart contract to freeze his tokens — and threatened to 'burn' them — after he refused to mint USD1 stablecoin on Tron.

Tron founder Justin Sun, the early anchor investor whose $45 million in 2024–25 transformed the Trump family's World Liberty Financial from a slow-selling token launch into a $550 million crypto venture, sued World Liberty in federal court on Tuesday. The 52-page complaint, filed in the U.S. District Court for the Northern District of California, alleges that World Liberty's principals secretly added a "blacklisting" backdoor to the company-controlled $WLFI smart contract in August 2025 and used it to freeze roughly 2.9 billion of Sun's tokens — preventing him from selling a single one even after the token's September 1 transferability date — while threatening to permanently "burn" his holdings if he tried to enforce his rights through legal action.

The case — Yuchen "Justin" Sun, Blue Anthem Limited, and Black Anthem Limited v. World Liberty Financial LLC, Case No. 3:26-cv-03360 — names World Liberty's LLC entity as the sole defendant. Trump family members are not named, though the complaint repeatedly states that Sun invested "because of the Trump family's association with the project" (Para. 3) and that World Liberty's operators, including co-founder Chase Herro, "see the project as a golden opportunity to leverage the Trump brand to profit through fraud" (Para. 4). The plaintiffs are represented by Cahill Gordon & Reindel and Keker Van Nest & Peters.

What the contract guaranteed

The centerpiece of the complaint is the November 25, 2024 Token Purchase Agreement, signed when Sun made his initial $30 million purchase. The TPA, the complaint says (Para. 8), "contained representations by World Liberty making clear that (i) World Liberty would have no centralized authority over $WLFI tokens; and (ii) the tokens were expected to become tradable in the future." The contract specifically promised Sun would "acquire valid marketable title to the Purchased Tokens, free and clear of any pledge, lien, security interest, encumbrance, claim or equitable interest."

Sun followed the November 2024 anchor investment with another $15 million in January 2025. World Liberty appointed him as an advisor and granted him an additional one billion $WLFI tokens as compensation for the role, the complaint states. According to Para. 7, those investments transformed the project: World Liberty had sold only "$12 million worth of tokens after 24 hours, and only $22 million worth in the first month" before Sun came in. After Sun, World Liberty raised approximately $550 million through $WLFI sales — "a 2,400% increase since Mr. Sun lent his name and credibility to the project."

The alleged backdoor

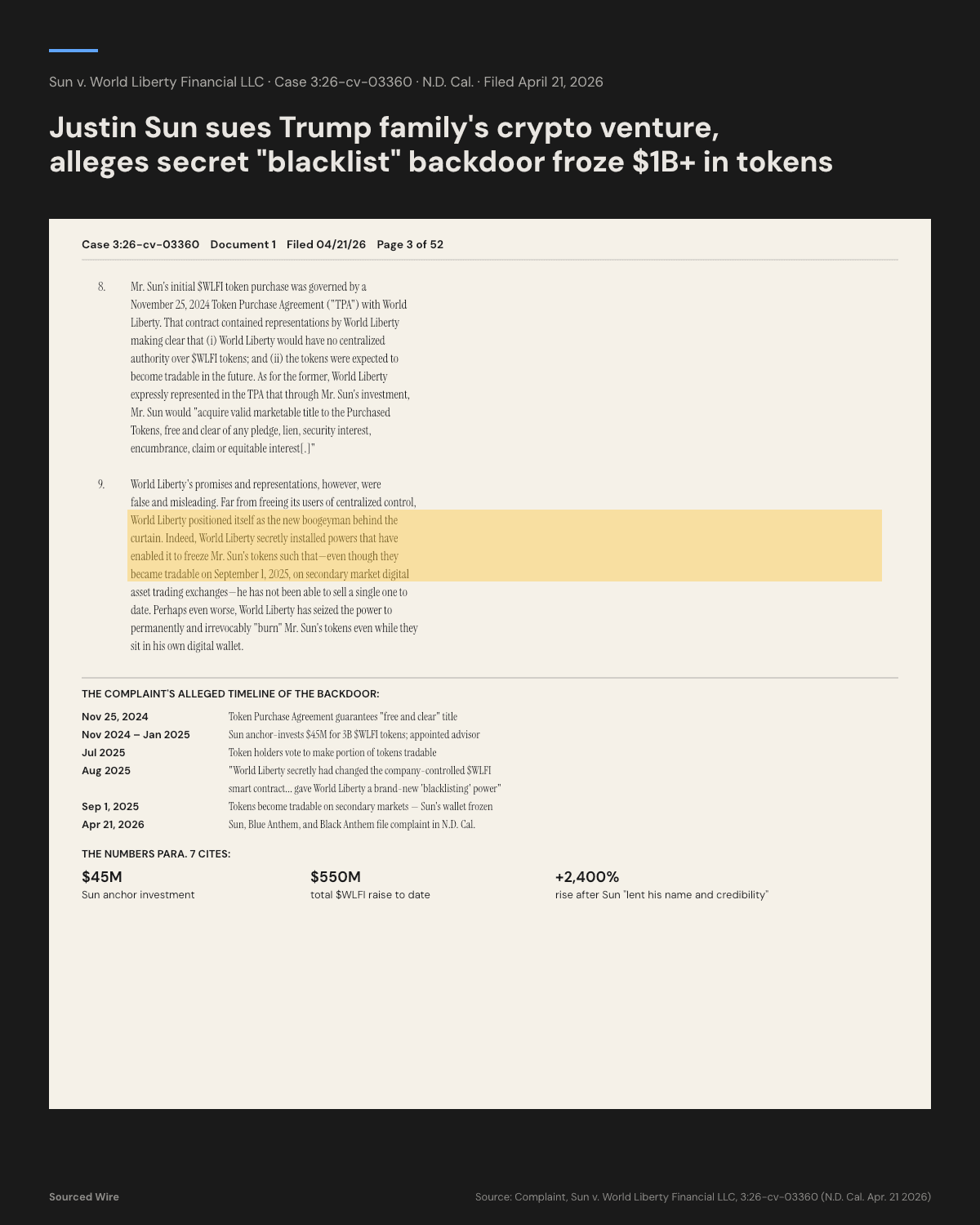

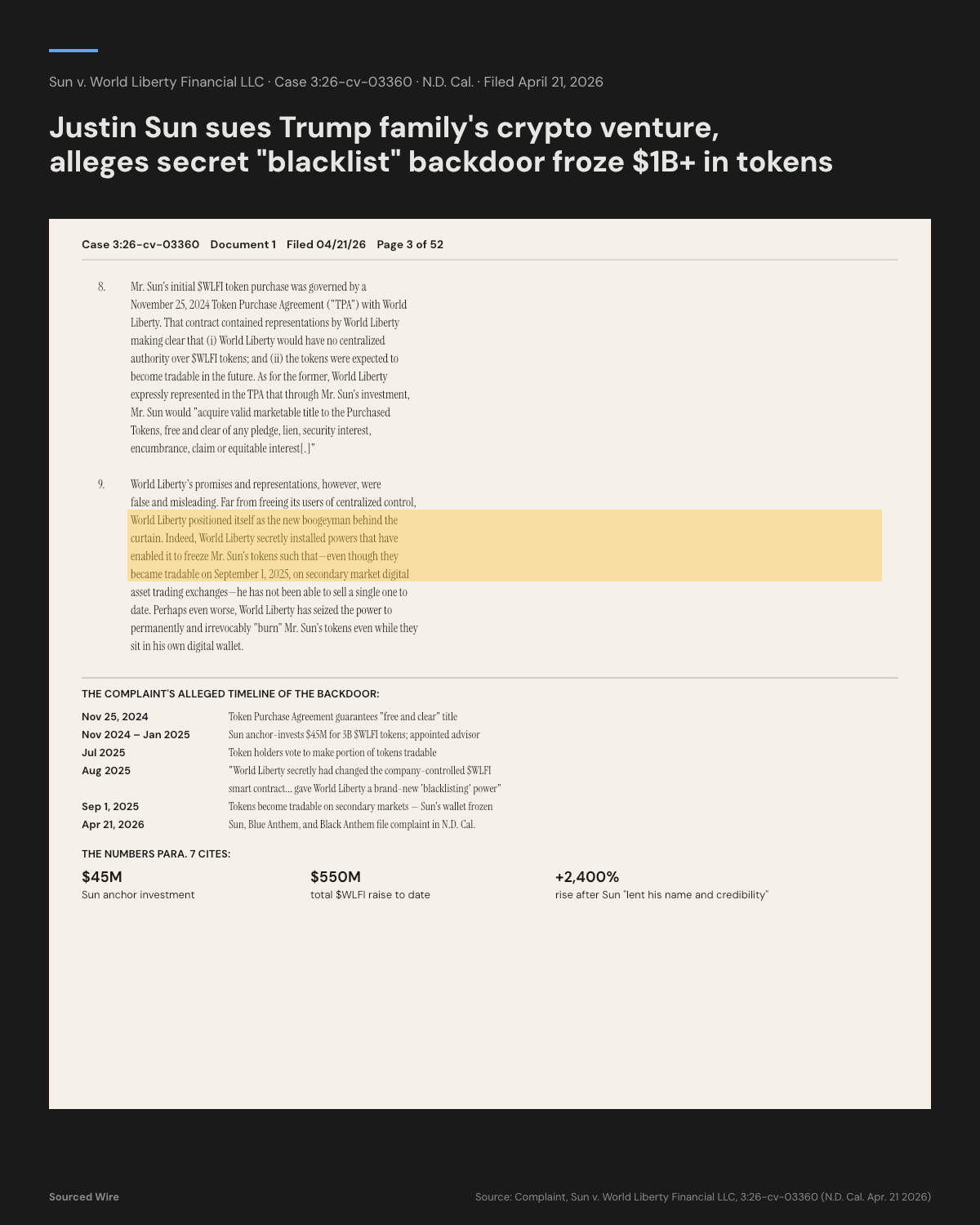

The complaint describes the alleged contract change in Para. 10: "In August, shortly before the first tranche of $WLFI tokens was set to become tradable in September, Plaintiffs learned that World Liberty secretly had changed the company-controlled $WLFI smart contract used to deploy the tokens in a way that gave World Liberty a brand-new 'blacklisting' power enabling it to restrict the transfer of users' tokens. There was no governance proposal (let alone a vote of token holders) on whether World Liberty should have this power, nor did World Liberty announce to token holders what the company was doing. World Liberty simply took the power for itself."

In Para. 9, the complaint borrows World Liberty's own marketing language to make its point: World Liberty's CEO had publicly described DeFi companies as freeing users from "the big boogeyman behind the curtain." The complaint replies: "World Liberty positioned itself as the new boogeyman behind the curtain." Even after the September 1, 2025 unlock date that made $WLFI tokens tradable on secondary markets, the complaint says, Sun "has not been able to sell a single one to date."

The USD1 leverage

The complaint frames the alleged token freeze as leverage in a separate dispute over World Liberty's USD1 stablecoin. According to Para. 11, USD1 "had faced underwhelming retail demand," and World Liberty's principals "had been trying to convince Mr. Sun to 'mint' USD1 — in other words, to create USD1 by purchasing it with a corresponding number of U.S. dollars — and promote it for use on the blockchain that Mr. Sun developed, namely TRON." When Sun, by August 2025, had not agreed to provide that capital, the complaint says, "World Liberty imposed special restrictions on the transferability of Mr. Sun's tokens ahead of the September unlock" — restrictions Sun argues were a coercion mechanism, not a routine compliance measure.

Causes of action and relief

The complaint asserts breach of contract, fraud in the inducement, conversion, unjust enrichment, and declaratory relief. It seeks an order requiring World Liberty to unfreeze Sun's tokens immediately, damages to be determined at trial, and an injunction against burning, destroying, or tampering with the holdings. The case has been assigned a 04/21/26 filing date but no judge or trial date as of the docket's first publication.

Context: WLF and the Trump portfolio

World Liberty Financial is one of the Trump family's most prominent post-2024 commercial ventures. The project markets itself as a DeFi platform — a category the complaint says, citing World Liberty's own representations, was supposed to ensure "no one's ever going to tell you that your account is shut down" and "no one's ever going to tell you who and why and what money you can send." Sun, who in addition to founding Tron has been a vocal Trump supporter, says he "tried in good faith to resolve this situation" before filing. "All I want," he wrote on X on Tuesday, "is to be treated the same as every other early investor."