HHS-OIG: 79% of Medicare Part D Enrollees Are in Vertically Integrated Plans and Pay ~40% More Out of Pocket Without Financial Assistance

A May 15 HHS Office of Inspector General data snapshot finds that 11 vertically integrated organizations — sponsors that also own a pharmacy benefit manager — covered 79% of Medicare Part D's 54.6 million enrollees in 2023, and that enrollees without financial assistance paid nearly 40% more in out-of-pocket drug costs than enrollees in non-integrated plans, despite paying lower monthly premiums.

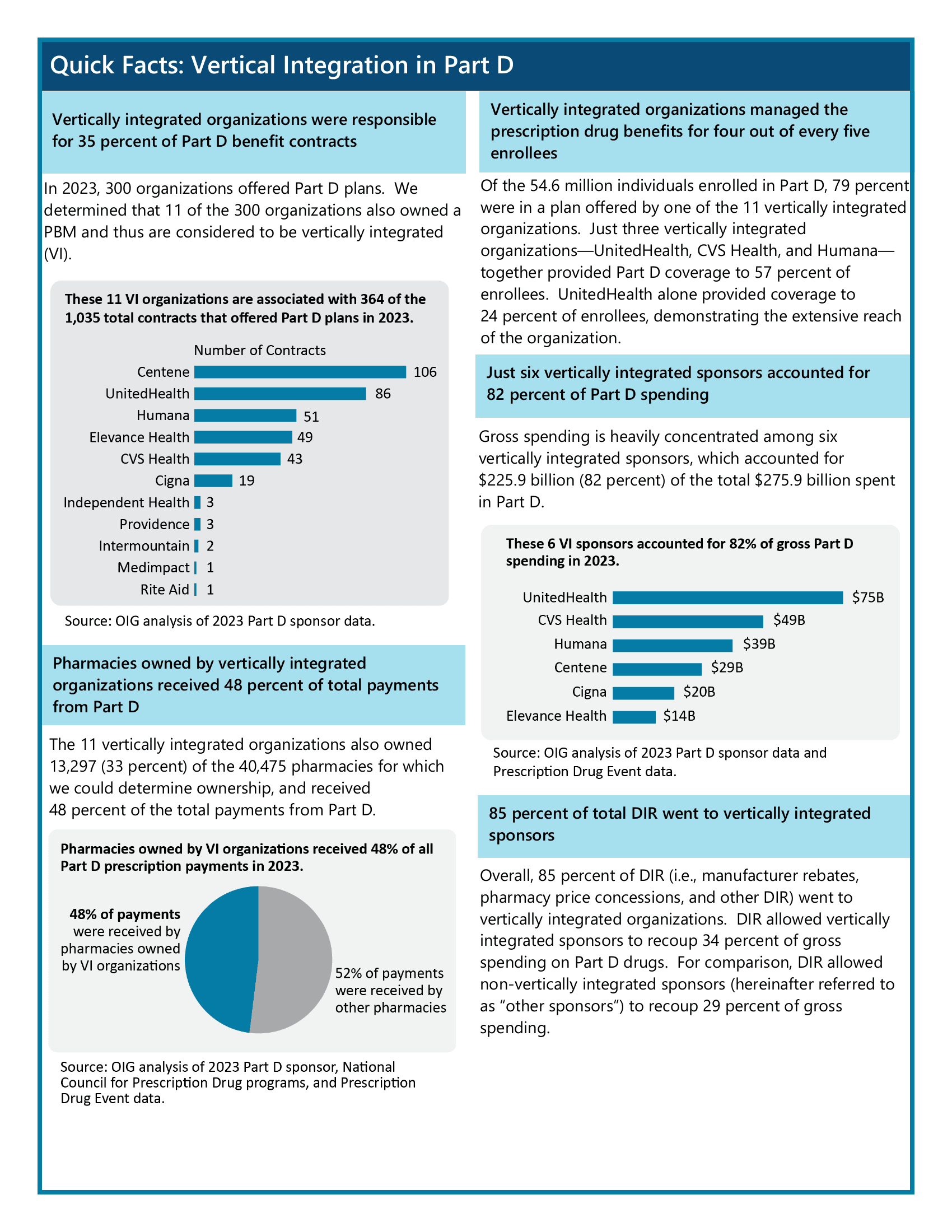

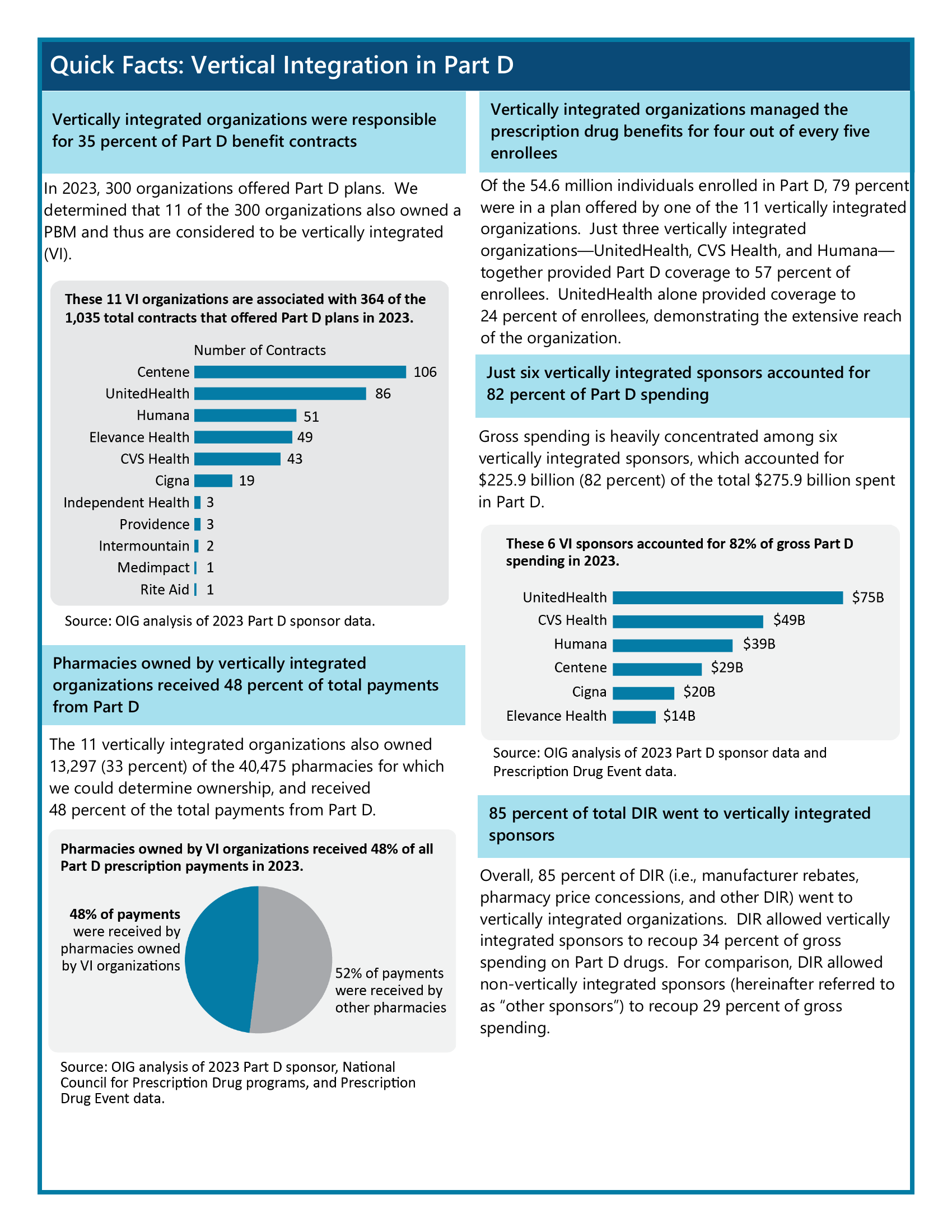

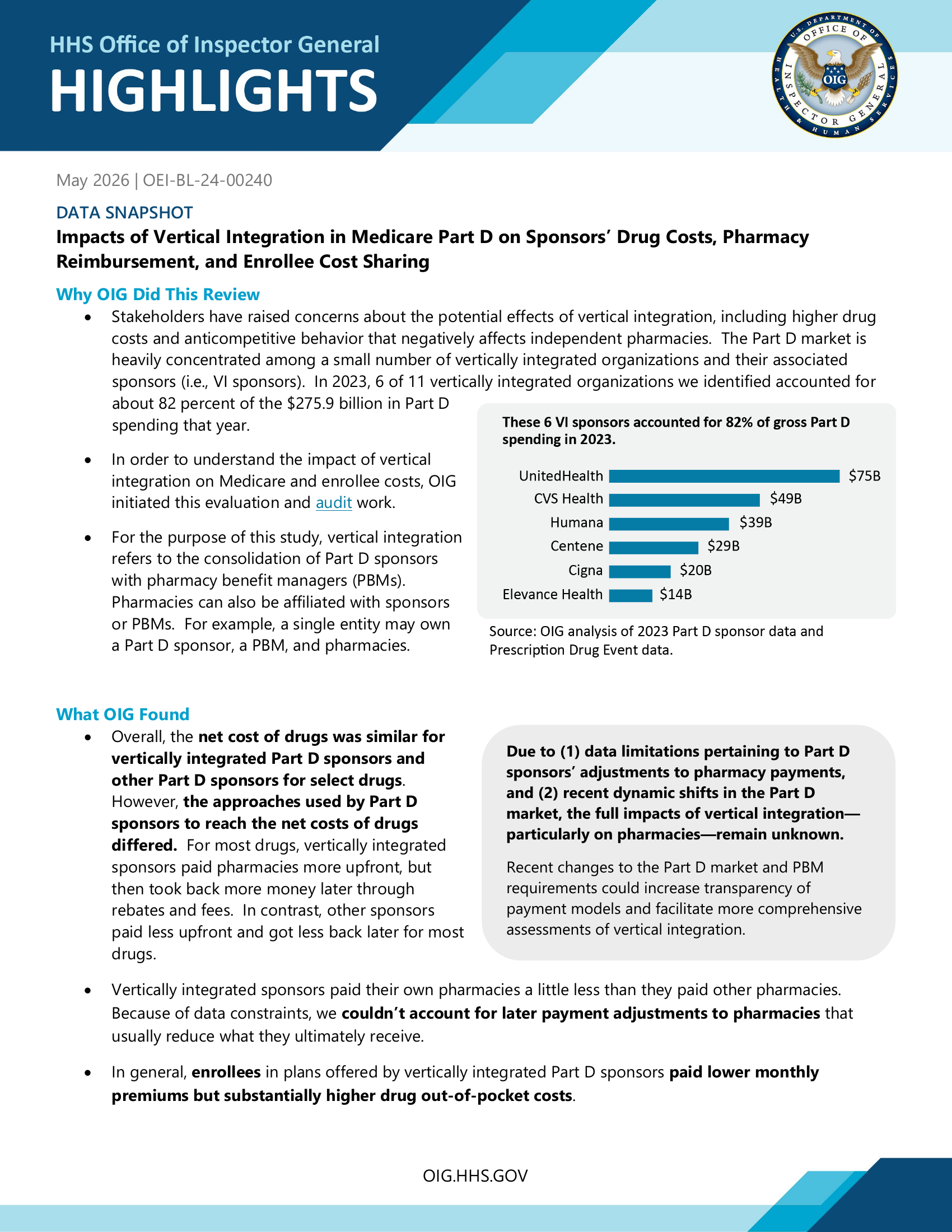

The Department of Health and Human Services' Office of Inspector General published a data snapshot on May 15 quantifying, for the first time at this level of detail, how vertical integration has reshaped the Medicare Part D prescription drug benefit. The headline finding: in 2023, just 11 of the 300 organizations offering Part D plans also owned a pharmacy benefit manager, and those 11 organizations covered 79 percent of the program's 54.6 million enrollees. Six of them — UnitedHealth, CVS Health, Humana, Centene, Cigna, and Elevance Health — accounted for 82 percent of the program's $275.9 billion in gross spending.

The report (OEI-BL-24-00240) is a point-in-time baseline, not an audit; OIG flags throughout that incomplete pharmacy payment data limits how far conclusions can be pushed. But on what the data does show, the snapshot lands a specific, quantified finding that hadn't been published before: enrollees in vertically integrated plans pay less up front and more at the counter.

What vertical integration looks like

A vertically integrated Part D sponsor is one whose parent company also owns the pharmacy benefit manager (PBM) that negotiates drug prices on its behalf — and, in most cases, owns retail, mail-order, or specialty pharmacies as well. UnitedHealth owns OptumRx; CVS Health owns Caremark and the CVS retail and specialty chains; Cigna owns Express Scripts and Accredo. OIG identified 11 such organizations across the 2023 Part D market.

By spending, concentration is steeper than by contract count. UnitedHealth alone accounted for $75 billion in gross Part D spending in 2023; CVS Health $49 billion; Humana $39 billion; Centene $29 billion; Cigna $20 billion; Elevance Health $14 billion. The other five vertically integrated organizations — Independent Health, Providence, Intermountain, Medimpact, and Rite Aid — combined for the remainder. By contract count, Centene led with 106 of the 1,035 Part D contracts on offer.

The 11 integrated organizations also owned 13,297 of the 40,475 pharmacies (33 percent) for which OIG could determine ownership, and those owned pharmacies received 48 percent of all Part D prescription payments in 2023.

Premiums down, out-of-pocket up

OIG's enrollee-cost finding is the part of the report most directly visible to seniors. Monthly premiums for the drug benefit portion of plans offered by vertically integrated sponsors were lower across both major plan types:

| Plan type | VI sponsor premium | Other sponsor premium |

|---|---|---|

| Medicare Advantage (drug-benefit portion) | $10 | $20 |

| Standalone Prescription Drug Plan | $38 | $54 |

Out-of-pocket spending moved the other way. Looking at a purposive sample of 60 high-cost or high-use drugs, OIG found that enrollees without financial assistance paid nearly 40 percent more, overall, in drug out-of-pocket costs when their plan was offered by a vertically integrated sponsor. That gap held for 52 of the 60 drugs in the sample.

Enrollees who did receive financial assistance — about 41 percent of the study population, mostly through the low-income subsidy — paid roughly 5 percent more in VI plans, a much smaller difference.

OIG offers a structural reason the two numbers move in opposite directions. Vertically integrated sponsors collect substantially more in direct and indirect remuneration (DIR) — the manufacturer rebates and pharmacy fees that flow back to sponsors after the point of sale. Eighty-five percent of all DIR went to the 11 vertically integrated organizations. Because DIR offsets a plan's costs, sponsors can use it to fund lower premiums. But under the Part D rules in effect during the study period, enrollee cost-sharing was calculated from the gross point-of-sale price, not the net post-rebate price. The result: a plan can both quote a low premium and produce a high out-of-pocket charge at the pharmacy counter, because the rebates that reduce cost for the plan don't pass through to the enrollee at fill time.

Net drug costs were similar — the routing was different

For the 60 drugs OIG sampled, the net cost paid by vertically integrated sponsors and other sponsors was within 1 percent of each other. Brand-only drugs came out 0.3 percent lower under VI sponsors; multiple-source (generic-eligible) drugs came out 2 percent lower.

But the path to that similar net cost was different. For 41 of the 60 drugs, vertically integrated sponsors reimbursed pharmacies more at the point of sale than other sponsors did. For 36 of 60, they then clawed back more after the point of sale in DIR fees and rebates. Other sponsors generally did the inverse — pay less up front, take back less later.

OIG also looked at how vertically integrated sponsors paid their own pharmacies versus unaffiliated ones. At the point of sale, VI sponsors paid affiliated pharmacies 4 percent less than unaffiliated pharmacies on average; the spread was 3 percent for brand-only drugs and 8 percent for multiple-source drugs. Both flows landed above the National Average Drug Acquisition Cost (NADAC), which OIG used as a proxy for pharmacy acquisition cost. VI sponsors reimbursed their own pharmacies 11 percent above NADAC; unaffiliated pharmacies 16 percent above.

Whether those point-of-sale differences survive post-sale DIR adjustments OIG could not determine. Sponsors do not report pharmacy DIR separately from other DIR at the drug level, so the agency could not trace flows from specific pharmacies to specific sponsors. That gap is the single most-cited limitation in the report.

Why now

OIG launched the evaluation after stakeholder pressure on PBM concentration intensified. The report cites an April 2025 letter from the National Association of Attorneys General to Congress charging that PBM ownership of affiliated pharmacies "has exacerbated the problem of manipulated prices and unavailability of certain prescription medications," and a Federal Trade Commission finding that approximately 10 percent of independent retail pharmacies in rural areas closed between 2013 and 2022.

The Part D rules have already begun to shift in ways that OIG flags will change the picture. As of January 2024, pharmacy price concessions must be reflected at the point of sale — which could lower what enrollees pay at fill time. As of January 2025, annual enrollee out-of-pocket drug spending is capped at $2,000. By April 2028, CMS must finalize standards for "reasonable and relevant" contract terms between sponsors and pharmacies, including fair reimbursement rates; sponsors must implement those standards by January 2029, and CMS will launch a complaint process under anti-retaliation protections. Beginning January 2028, PBMs will no longer be permitted to receive compensation tied to drug list prices or rebate amounts — only flat service fees.

OIG flags that it is currently conducting an audit of the contract arrangements between several vertically integrated entities and pharmacies in 2023 and 2024, and that the audit work will complement this evaluation when it is released.

Methodology notes

OIG identified vertically integrated organizations using 2023 DIR submission data, contract information, financial reporting documentation, and sponsor bid submissions, then matched pharmacy ownership through National Council for Prescription Drug Programs data and pharmacy websites. Ownership data was determinable for pharmacies accounting for 73 percent of Part D expenditures.

The 60-drug sample was constructed by taking the top 20 drugs each by total expenditure, total enrollees, and average cost per enrollee. Comparisons of sponsor costs, point-of-sale payments, and enrollee out-of-pocket costs apply only to that sample and are not generalizable to all Part D drugs.

The four findings OIG could and could not draw are spelled out plainly in the conclusion section: drug net costs were similar between VI and other sponsors; VI sponsors paid their own pharmacies a little less at the point of sale than they paid unaffiliated pharmacies; enrollees in VI plans had lower premiums but higher out-of-pocket costs for the sampled drugs; and the full effect of vertical integration on pharmacy net payments could not be determined because of DIR data limitations.